Indicators on Tulsa Bankruptcy Filing Assistance You Need To Know

Indicators on Tulsa Bankruptcy Filing Assistance You Need To Know

Blog Article

Getting My Tulsa Ok Bankruptcy Attorney To Work

Table of ContentsChapter 7 Bankruptcy Attorney Tulsa for BeginnersThe Ultimate Guide To Tulsa Bankruptcy LawyerThe smart Trick of Affordable Bankruptcy Lawyer Tulsa That Nobody is DiscussingChapter 7 Bankruptcy Attorney Tulsa for DummiesHow Tulsa Bankruptcy Lawyer can Save You Time, Stress, and Money.More About Bankruptcy Lawyer Tulsa

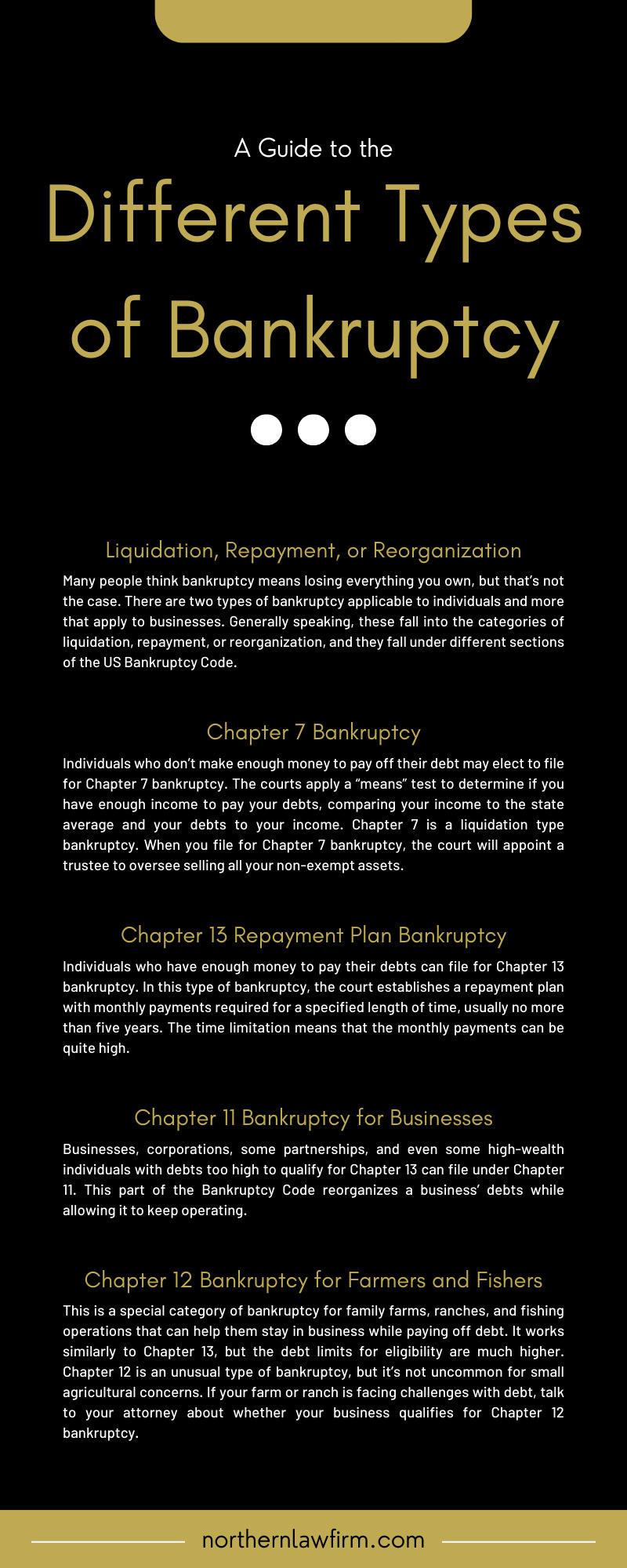

People need to make use of Phase 11 when their debts go beyond Chapter 13 debt limitations. It hardly ever makes feeling in various other circumstances but has a lot more options for lien stripping and cramdowns on unprotected parts of protected lendings. Phase 12 personal bankruptcy is developed for farmers and fishermen. Chapter 12 settlement strategies can be more flexible in Chapter 13.The methods examination takes a look at your typical monthly income for the 6 months preceding your filing day and contrasts it versus the typical income for a similar family in your state. If your revenue is below the state median, you automatically pass and do not need to complete the whole type.

The debt limitations are listed in the graph above, and existing amounts can be validated on the U.S. Courts Phase 13 Bankruptcy Basics webpage. Find out more about The Way Test in Chapter 7 Insolvency and Financial Debt Limits for Chapter 13 Personal bankruptcy. If you are wed, you can apply for insolvency collectively with your partner or independently.

Filing personal bankruptcy can aid an individual by discarding financial obligation or making a strategy to settle financial debts. A personal bankruptcy instance generally begins when the debtor submits a request with the insolvency court. There are different types of bankruptcies, which are usually referred to by their chapter in the U.S. Personal Bankruptcy Code.

If you are facing financial challenges in your individual life or in your service, chances are the principle of filing insolvency has actually crossed your mind. If it has, it also makes good sense that you have a lot of bankruptcy concerns that need solutions. Lots of people in fact can not answer the question "what is personal bankruptcy" in anything except basic terms.

If you are facing financial challenges in your individual life or in your service, chances are the principle of filing insolvency has actually crossed your mind. If it has, it also makes good sense that you have a lot of bankruptcy concerns that need solutions. Lots of people in fact can not answer the question "what is personal bankruptcy" in anything except basic terms.Many individuals do not understand that there are a number of kinds of bankruptcy, such as Phase 7, Phase 11 and Phase 13. Each has its benefits and obstacles, so understanding which is the best alternative for your existing scenario along with your future recuperation can make all the distinction in your life.

Getting The Bankruptcy Lawyer Tulsa To Work

Phase 7 is called the liquidation personal bankruptcy chapter. In a chapter 7 insolvency you can get rid of, wipe out or discharge most sorts of debt. Examples of unsecured financial debt that can be eliminated are bank card and clinical costs. All sorts of people and business-- individuals, couples, firms and collaborations can all submit a Chapter 7 insolvency if eligible.

Numerous Phase 7 filers do not have a lot in the means of assets. They might be occupants and own an older cars and truck, or no auto at all. Some cope with parents, buddies, or siblings. Others have residences that do not have much equity or remain in major requirement of repair.

The quantity paid and the duration of the plan depends upon the borrower's residential property, mean income and expenditures. Financial institutions are not permitted to go after or maintain any type of collection tasks or legal actions during the case. If successful, these financial institutions will go to this site certainly be cleaned out or released. A Phase 13 insolvency is really effective due to the fact that it gives a system for debtors to avoid repossessions and sheriff sales and stop repossessions and energy shutoffs while catching up on their protected financial debt.

The Main Principles Of Tulsa Bankruptcy Filing Assistance

A Phase 13 situation may be helpful because the debtor is allowed to obtain captured up on home mortgages or automobile financings without the danger of repossession or foreclosure and is enabled to keep both excluded and nonexempt property. The borrower's strategy is a file outlining to the personal bankruptcy court how the debtor proposes to pay current costs while paying off all the old financial debt equilibriums.

The Only Guide to Chapter 13 Bankruptcy Lawyer Tulsa

Sometimes it is better to prevent bankruptcy and work out with creditors out of court. New Jacket also has a different to personal bankruptcy for services called an Job for the Benefit of Creditors and our law office will certainly discuss this option if it fits as a possible technique for your business.

We have actually developed a tool that aids you select what phase your documents is probably to be filed under. Click on this link to make use of ScuraSmart and locate out a feasible solution for your financial debt. Lots of people do not recognize that there are numerous kinds of personal bankruptcy, such as Chapter 7, Phase 11 and Phase 13.

Below at Scura, Wigfield, Heyer, Stevens & Cammarota, LLP we manage all types of insolvency cases, so we are able to address your personal Discover More bankruptcy concerns and help you make the most effective choice for your case. Below is a quick look at the financial debt alleviation choices available:.

The 7-Second Trick For Chapter 13 Bankruptcy Lawyer Tulsa

You can just apply for bankruptcy Before declaring for Chapter 7, at the very least among these should be real: You have a great deal of financial debt earnings and/or assets a creditor could take. You shed your copyright after being in a mishap while without insurance. You need your license back (Tulsa OK bankruptcy attorney). You have a great deal of financial debt near to the homestead exemption amount of in your house.

The homestead exemption quantity is the better of (a) $125,000; or (b) the region median list price of a single-family home in the preceding schedule year. is the quantity of money you would keep after you offered your home and paid off the home mortgage and other liens. You can find the.

Report this page